What Every Pharmacist Needs To Know About The PBM Playbook

Carley’s note: Hello, my sweet pharmacy phriends! Today, we’re going to cover a few topics that honestly keep me awake tossing and turning at night. It’s become more difficult than ever to be a successful pharmacy owner in an era that feels riddled with financial landmines. For that reason, I wrote today’s article to get a little bit off of my chest, and hopefully voice some things you’ve been thinking about too. Without further ado…

You see, I LOVE being a pharmacist. My colleagues around me love being pharmacists. I’ve seen what good pharmacists can do for a community and will always defend the fact that we are an essential part of keeping patients healthy…so why are so many pharmacies struggling to keep their doors open?

To get to the bottom of that, we need to understand the often invisible powers at play behind the scenes. That’s right; today, we’re talking about Pharmacy Benefit Managers (PBMs), reimbursements, and the current fight for fairness within them. Before we dive into the really juicy stuff, though, we need to take a look at the past and understand what a PBM is and what its role was supposed to be (and don't worry, as tempting as it is, this won't be a name-calling session 😉).

What is a PBM?

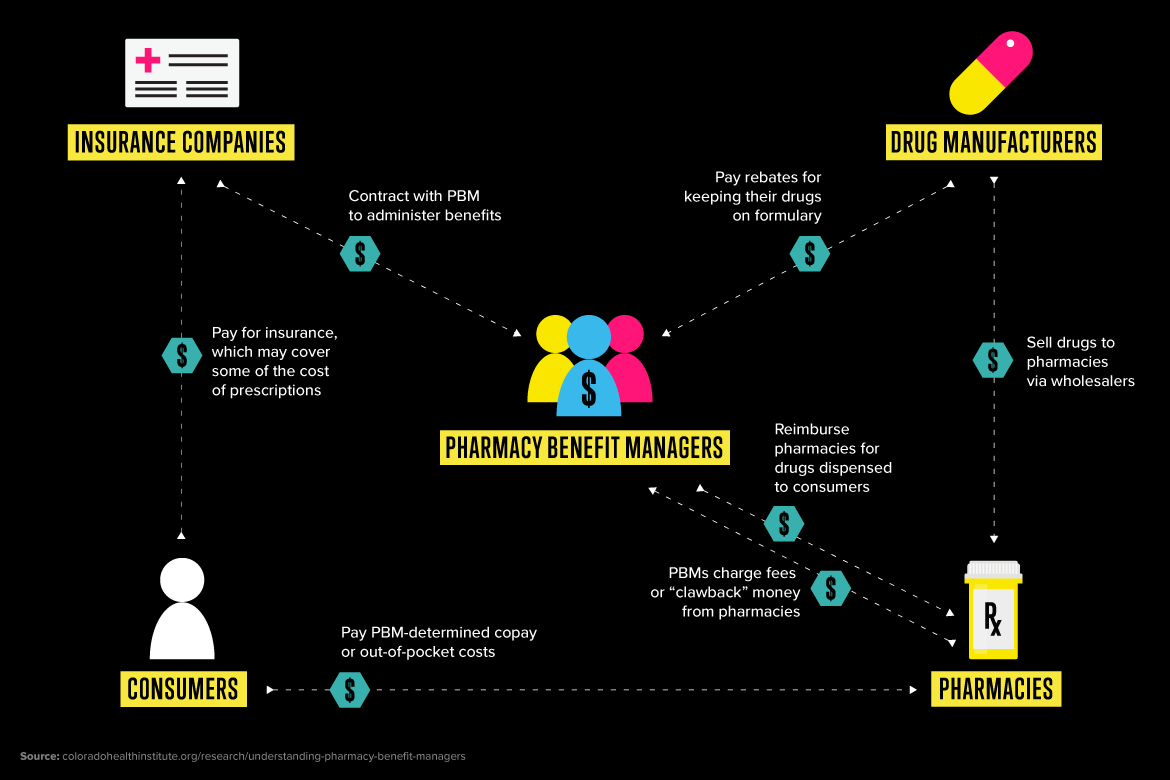

(Image)

A PBM, or Pharmacy Benefit Manager, is essentially a middleman hired by health insurance plans to manage their prescription drug benefits. Think of them as the "HR department" for your insurance company's pharmacy claims. This system didn't appear overnight or even recently, though. It began back in the 1960s and 70s, when PBMs served as simple claims processors, handling paperwork for insurers. In fairness, they’ve always done this job pretty well! It’s thanks to this system that pharmacies are paid almost immediately when they adjudicate a claim, compared to medical insurance, which can take weeks to reimburse a clinic. This role changed in the 1990s, as new drugs and rising prices began to strain healthcare budgets. From there, PBMs took on new, more controlling roles such as creating drug formularies and negotiating rebates with manufacturers, all in the name of keeping “spending down”. As the PBMs were able to gain control over these tools, they also were able to grow their power…and profits. This, unfortunately, set us up for two trends that would be present from the 2000s onward.

First, we saw the market begin to consolidate. Smaller PBMs were bought out by larger ones, shrinking what was once a pretty diverse marketplace down to only a handful of “big boys” who now control almost all of the prescriptions across the country. With that much control over the market, the second and more significant evolution started…vertical integration. These giant PBMs started to merge with, or just straight up buy, companies up and down the healthcare supply chain (let’s be real, this was really just to squash competition). Don’t worry, we’re going to talk allllll about that later.

This brings us to today, where the modern healthcare landscape is a little bit of a fiasco. In our current era, a single corporation can own a major insurance plan, one of the country’s largest PBMs, its own chain of retail, mail-order, specialty pharmacies, and even drug manufacturing. That one corporation can now produce its own “Value Brand” versions of specialty drugs like biosimilars. This allows them to create a closed-loop system in which their own PBM only covers THEIR brand of biosimilar, completely eliminating competition from every step of the process.

The result of all of this is the industry behemoths we see today, companies that both compete with AND determine the financial terms to nearly every pharmacy you pass. Kind of crazy, right? So how does this immense power actually hit your pharmacy’s bottom line? It's all in the reimbursement math. While we've covered the basics of pharmacy finance before, today we’re focusing on how PBMs have turned that simple formula into a weapon.

How are pharmacies reimbursed?

To start, we have to understand how to calculate the reimbursement for a prescription:

Pharmacy Reimbursement = (Ingredient Cost) + (Dispensing Fee) - (Patient Copay)

So, how does a pharmacy actually make money? The goal is to generate Gross Profit. Simply put, that’s the money left over after you subtract what you paid for the drug (your Actual Acquisition Cost) from the total Revenue you receive (the PBM payment plus the patient’s copay). This gross profit is the critical fund that covers salaries, rent, utilities, and everything else needed to keep the lights on.

This is where the logic of the reimbursement formula breaks down. To understand how, we need to be crystal clear about two completely different prices for the exact same generic drug:

Actual Acquisition Cost (AAC): This is the real price. It's what a pharmacy actually pays a wholesaler for a medication.

Maximum Allowable Cost (MAC): This is the PBM's price. It's a price ceiling created entirely by the PBM in a black box, with no transparency into how it's calculated or updated. Even worse, they can technically anchor this MAC price to ANY low cost they find publicly - think about direct-to-consumer pharmacy prices, which at times are lower than pharmacy acquisition prices - and apply it to everyone.

Me trying to make the PBM reimbursement math make sense. (Image)

Here’s the really crucial part: in the reimbursement formula, the PBM ignores the pharmacy's Actual Acquisition Cost and uses its own MAC price as the "Ingredient Cost."

That’s the moment we’re forced to lose money. On purpose. The PBM’s MAC price is often set below what any pharmacy can actually buy the drug for. So even if the math seems to result in a "Gross Profit," that profit is based on a fictional number created by the PBM, not the real-world cost of the drug. Not cool.

Most PBMs do offer a “solution” for this - a MAC Appeal Process. Seems like a great idea, but unfortunately, most PBMs have created policies that make getting the payment corrected basically impossible. From short appeal windows to a complete lack of transparency, most appeals aren’t successful, forcing the pharmacy to eat the cost after wasting valuable time on the process. I can personally attest that I have NEVER had a successful MAC appeal…I promise I will come back and update this article if it ever happens.

Beyond the MAC

I wish our reimbursement problem stopped there, but to get a true picture of this crisis, we have to understand that even the initial payment received by the pharmacy is rarely the final story. These are honestly the tactics that caused me to toss and turn at night, wanting to write this in the first place:

Spread Pricing: This is when a PBM charges a health plan, like Medicaid, significantly more than it pays the pharmacy for the exact same medication, pocketing the difference as profit.

Clawbacks: If a patient’s copay happens to be higher than the medication’s MAC plus dispensing fee, the PBM will “claw back” the excess profit from the pharmacy, even though the pharmacy had nothing to do with setting either price (Seem fair to you? Yeah, me neither).

Direct and Indirect Remuneration Fees (DIR): This is easily the most damaging of all. Depending on the insurance plan, it takes one of two soul-crushing, agonizing forms:

The Retroactive Model (Most Commercial Plans): The PBM takes money back months after a prescription is filled. A claim that looked profitable at the time of dispensing can suddenly become a money-loser, leaving the pharmacy owner to never truly know their prescription profits.

The Point-of-Sale Model (Medicare Part D since 2024): After a CMS rule change in 2024, PBMs now build these fees directly into the initial payment. This eliminates the retroactive surprise but results in drastically lower upfront reimbursements that still ultimately squeeze a pharmacy's daily cash flow…so did they really get rid of them…

PBMs justify both of these models by claiming the fees are tied to a pharmacy’s "quality metrics" like medication adherence scores calculated from data the PBMs themselves control and often refuse to share. This creates an impossible system where pharmacies are graded and financially penalized based on metrics they were never even told about. All of this while they incentivize pharmacies to refill prescriptions as early and frequently as possible, often for 90 to 100-day supplies, resulting in their “quality metrics” not even being accurate representations of a patient’s current adherence or health status.

But to see the real-world damage of the retroactive model in action, let's put some numbers to it with a common prescription!

A Prescription’s Reimbursement Journey

Our guinea pig today is a very common friend: Lisinopril 10mg. Should be pretty simple, right?

The Illusion: What You Think You Made

Your favorite patient, Mary, comes in and hands you her prescription for lisinopril 10 mg, with a quantity of 30 tablets. Your actual cost to dispense this prescription is $1.50. You bill her insurance and get a paid claim - Mary is responsible for a $1.00 copay, and the PBM paid according to their MAC price of $2.00. The total revenue you’ve collected is $3.00 (PBM payment + Patient Copay). On paper, the math looks a little like this:

$3.00 (Total Revenue) - $1.50 (Actual Cost) = $1.50 Gross Profit

Altogether, you’ve made $1.50 to keep the lights on and pay your staff. It’s a little tight, but over the course of hundreds of prescriptions, it could add up. And hey, a profit is a profit, right?

The Reality: What You Actually Lost

Unfortunately, this is where the PBM playbook comes in. Three to six months later, you see the DIR fees get taken back. That single lisinopril prescription you filled ages ago gets hit with a retroactive $1.75 fee. Now, the real math shakes out to:

$1.50 (Gross Profit) - $1.75 (DIR Fee) = -$0.25 Net Loss

You ended up paying THEM 25 cents for the privilege of filling that prescription. Let that sink in. Now, imagine this happening on hundreds, or even thousands, of prescriptions a month. It’s the classic death by a thousand cuts; one underreimbursed claim won’t close your pharmacy…but hundreds of them a month just might. That's also just the DIR fee! We're not even counting the other little nicks and cuts we talked about, like direct clawbacks that bleed you out on other claims.

The True Cost of PBM Business Models

Okay, so now we see how the money works…or rather, how it doesn't. Now, let's connect the dots. How does this financial squeeze connect to the PBMs’ broader strategy of controlling the entire prescription process - from which drugs you can dispense, to where your patients can go, and even how much they ultimately pay out-of-pocket?

A key strategy that has unfortunately reshaped the healthcare landscape that I mentioned previously is vertical integration, which is what happens when a single healthcare entity owns the insurance plan, the PBM, its own chain of pharmacies, and potentially even manufacturing capabilities. It’s like the referee in a basketball game also owning one of the teams. This business model creates massive conflicts of interest that allow PBMs to engage in practices like patient steering.

Your computer screen when trying to get a paid claim for Mary’s specialty prescription. (Image)

Let’s go back to our prescription example. Remember Mary, the patient whose lisinopril prescription we just lost money on? Well, a few months later, her doctor prescribed a new specialty drug for her rheumatoid arthritis. Mary trusts you and wants to continue using your pharmacy, but when you try to fill it, the claim is rejected. The reason? The PBM that manages Mary’s insurance has mandated that this high-cost specialty drug can only be filled by their own mail-order specialty pharmacy. You are now completely locked out, and Mary is forced to leave the pharmacy team that she’s comfortable with for one of her most important medications (sorry, Mary, it’s not you, or us, it’s them). Mary’s story is a perfect example of patient steering, where she is steered away from her chosen home pharmacy to one owned by the PBM, eliminating both patient choice AND competition in one simple claim rejection. Not to mention, they may require that their manufactured version of the biosimilar be dispensed. So basically, not only are they taking money back at different points, but they’re literally taking your patients. Not nice.

This control also extends to which drugs get dispensed. Have you ever wondered why an insurance company forces you to dispense the brand name when a perfectly great generic already exists and is cheaper? PBMs can negotiate secret rebates from drug manufacturers in order to get a drug preferred status on a formulary, creating a “rebate wall”. Imagine a grocery store getting a huge kickback for stocking one specific brand of cereal, so they put it at eye level and hide all the cheaper (and sometimes better) options in the back. This can incentivize PBMs to favor higher-priced, brand-name drugs that offer a big rebate over cheaper, equally effective alternatives.

This control over pharmacies and formularies is all about maximizing the PBM’s profit, and that strategy extends directly to the patient’s side of the counter. They do this by twisting the very tools that patients try to use to manage their medication costs:

“Copay Accumulator” Programs: These stop the manufacturer's assistance from copay cards from counting toward a patient's deductible, leaving them with a massive, surprise bill later in the year because they are nowhere near meeting their out-of-pocket costs.

“Copay Maximizer” Programs: These are even more aggressive, draining a copay card’s entire value to ensure the PBM gets every dollar of the benefit, while none of it helps the patient reach their annual deductible.

Discount Cards: Even prescription discount cards have been wrangled in, with many now partnering directly with PBMs to absorb those “savings” into their own black box profit system.

These tactics create a system that’s complex, unpredictable, and downright financially dangerous. While the chaos is for sure a headache for every pharmacy, unfortunately, the damage isn’t distributed equally. Independent pharmacies, without the leverage of a national chain, face an entirely different level of risk.

How do PBMs impact independent pharmacies?

While the big national chains have plenty of lawyers and the scale to absorb these losses, independent pharmacies don't have that luxury. They don't have real negotiating power, so they're forced to sign whatever take-it-or-leave-it contract the PBM puts in front of them.

But what does "take-it-or-leave-it" actually mean? Think of it like this: a national chain negotiating with a PBM is like Walmart demanding a bulk rate from a supplier…their massive volume gives them leverage. An independent pharmacy is like a single customer trying to haggle at the checkout line, and the cashier doesn’t really care. The PBM can hand them a contract with the worst possible terms, and the pharmacy's only "choice" is to sign it or lose access to every patient that PBM covers, which could be half their business overnight. Even when independents try to team up in groups like Pharmacy Services Administrative Organizations (PSAOs), their collective power is still relatively tiny compared to that of a single PBM behemoth.

The result is that independents are locked into contracts with the lowest reimbursement rates and the most aggressive DIR fee structures. Unfortunately, many are already operating on razor-thin margins where a single below-cost reimbursement can be the difference between making payroll or not. When that same independent pharmacy decides to close its doors due to financial pressure, it has the potential to create a pharmacy desert, ultimately leaving its local community without access to care. This isn’t just a scary thought anymore; a recent report detailed that between 2018 and 2021, more US pharmacies actually closed than new pharmacies opened. Super scary to think about.

So, I guess by now you’re wondering…how do we fix it? Well, luckily, these issues (and their ultimate risk of a full-blown public health crisis) are starting to catch the attention of patients, providers, pharmacists, and legislators alike.

How to Get Involved in PBM Reform

The fight against unfair PBM practices isn’t a new one, and it’s gaining momentum. The single biggest victory came in 2020 with a landmark Supreme Court decision: Rutledge v. PCMA. For a long time, PBMs hid behind a federal law called ERISA, basically telling states, “You can't touch us.” The Supreme Court disagreed, unanimously at that. They ruled that ERISA does not preempt state laws, which essentially gave states the green light to step in and regulate these middlemen as they see fit. This was a HUGE power shift and opened the floodgates for state-level reform. Since then, we’ve seen states pass legislation involving greater transparency for MAC pricing, banning pharmacist “gag clauses” that prevent us from telling patients about cheaper cash prices, and prohibiting spread pricing to protect taxpayer dollars. Building on that momentum, the PBM crisis has finally caught the attention of Washington. Bipartisan federal bills, like the PBM Reform Act of 2025, are aiming to increase transparency and rein in the worst of these practices on a national scale.

While those wins are great, the good fight is far from over. PBMs continue to find new ways to squeeze pharmacies and find loopholes. This is where every pharmacist’s voice becomes SO critical in the fight. If this is something you’re passionate about, I’ve put together some resources for how to get involved:

Know Your Allies: Many pharmacy organizations that you may already be a part of often have a legislative team, or at least a dedicated legislative page or email subscriber list. This is an excellent way to stay up-to-date on current legislative happenings or opportunities to voice your opinion. Specifically, the National Community Pharmacists Association (NCPA) and the American Pharmacists Association (APhA) both have resources dedicated to tracking advocacy efforts. Don’t forget your state organizations, too!!

Know Your State’s Laws: Thanks to the Rutledge decision, your state has more power in its hands than ever. Research the specific PBM laws in your state. Is there a transparent MAC law? Are DIR fees regulated? If not, consider working with your legislators to draft legislation to introduce these things. Don’t wait for the change, go out there and be the change!

Make Your Voice Heard: Your story as a pharmacist is your most powerful weapon in this fight. Legislators need to hear from you and your colleagues, who are dealing with these issues firsthand; otherwise, they’re often naive to the day-to-day pains you’re feeling. You can use this site to find your local, state, and federal representatives, including their contact information, so that you can tell your story (seriously, we need all the help we can get)!

The Future of Drug Cost Transparency

Alas, our story doesn’t end there. A new wave of business models, in addition to the legislation we just talked about, is proving that the future could be different. These new models seem to put transparency ahead of secret profits. Examples such as Mark Cuban's Cost Plus Drug Company (which sells drugs at their actual acquisition cost plus a small, flat fee) and a growing number of transparent PBMs (which charge a flat admin fee instead of playing the spread pricing game) are proving that a different way may be possible. While these efforts are great, it’s important to remember that with increased transparency, PBMs are still able to weaponize this information for purposes such as MAC prices, like we mentioned earlier. For that reason, the role of reform in this fight simply can’t be understated.

Between continued advocacy and these new game-changers, the future of pharmacy doesn’t have to be defined by financial stress and crisis. It can be one where we are empowered to focus on what we do best - helping our patients and keeping our communities healthy.

The tl;dr of PBMs, Reimbursement, and the Fight for Fairness

PBMs went from simple claim processors in the 70s to the vertically integrated giants that now control the entire game, including which drugs are covered for our patients and which pharmacies they can use.

The reimbursement system right now is a black box. PBMs pay pharmacies based on their own secret MAC price, which most of the time is less than what was actually paid for the drug, forcing the pharmacy to dispense at a loss from the start.

Spread Pricing, Clawbacks, and DIR fees are basically the biggest nightmare. They allow PBMs to sneak secret profits for themselves, claw back any extra profits from pharmacies, and take extra metric-based fees from already low or non-existent profits. This turns what looked like profitable prescriptions at the time of dispensing into a money-losing one if done retrospectively.

The whole system is riddled with conflicts of interest. Vertical integration allows for patient steering to PBM-owned pharmacies and a “rebate wall” that is often in favor of expensive, high-rebate, brand-name drugs.

This financial squeeze often hits independent pharmacies the hardest. When they’re forced to close, it creates pharmacy deserts and turns a business problem into a public health problem.

The fight for fairness has been a long one, but it’s still going! The most powerful thing you can do is get informed and make your voice heard! Go do great things!